tnfd.global

Discussion paper on

Draft sector metrics

December 2023

For market consultation and feedback

SASB sectors:

Apparel and textiles (CG.1)

Construction materials (EM.2)

Infrastructure (IF.2)

Real estate (IF.3)

Draft sector metrics

For market consultation and feedback – December 2023

1

Contents

Introduction 2

Open for consultation 4

Consumer goods 6

Apparel & textiles 6

Proposed guidance on the application of the core

global disclosure metrics 6

Proposed core sector disclosure indicators and metrics 14

Proposed additional sector disclosure indicators and metrics 15

Extractives & minerals processing 16

Construction materials 16

Proposed guidance on the application of the core

global disclosure metrics 16

Proposed core sector disclosure indicators and metrics 24

Proposed additional sector disclosure indicators and metrics 25

Infrastructure 26

Infrastructure; Real estate 26

Proposed guidance on the application of the core

global disclosure metrics 26

Proposed core sector disclosure indicators and metrics 36

Proposed additional sector disclosure indicators and metrics 37

Glossary 39

References 44

This work is licensed under a

Creative Commons Attribution

4.0 International License.

Draft sector metrics

For market consultation and feedback – December 2023

2

Introduction

1 Including the GBF, ISSB IFRS-S1 and S2 standards; TCFD; Carbon Disclosure Standards Board (CDSB) and Sustainability Accounting

Standards Board (SASB); GRI, CDP and the European Financial Reporting Advisory Group (EFRAG); and corporate target setting methods

developed by the Science Based Targets Network (SBTN).

2 Taskforce on Nature-related Financial Disclosures (2022) A landscape assessment of nature-related data and analytics availability.

The TNFD Recommendations provide companies and

nancial institutions of all sizes with a risk management

and disclosure framework to identify, assess, manage

and, where appropriate, disclose nature-related issues.

This includes a set of recommended metrics to support

organisations’ assessment and disclosure of nature-

related dependencies, impacts, risks and opportunities.

The Taskforce’s approach to metrics is anchored in the

principles that metrics should be:

• Science-based and provide insights into the

consequences of business and nance activities;

• Be sensitive enough to reect change on an annual

basis;

• Relevant to the business model and value chain

of report preparers, recognising that issues within

sectors, business models and value chains can vary

signicantly;

• Proportionate, reecting the practical capacity and

cost constraints of report preparers to assemble,

assess and report information on an annual reporting

cycle;

• Decision-useful to the primary users of corporate

sustainability reports, oering current insights and

comparability within and across sectors;

• Subjectable to independent limited assurance in

the medium term; and

• Aligned to global and national policy goals

and targets, such as the indicators and metrics

in the Kunming-Montreal Global Biodiversity

Framework (GBF) and other international treaties

– as organisations are now aligning to the Paris

Agreement and net zero targets with respect to their

climate-related corporate disclosures – as well as

other standards and target setting frameworks.

1

The TNFD recognises that the scope, consistency

and accessibility of some nature-related data currently

available to some market participants means that

it is challenging to achieve all these principles

simultaneously.

2

To reconcile the large number of

indicators associated with nature-related issues, and the

needs of market participants for a small set of indicators

that can be compared and subjected to third-party

assurance on an annual basis as a key requirement for

disclosure, the TNFD has adopted a leading indicators

approach to measurement.

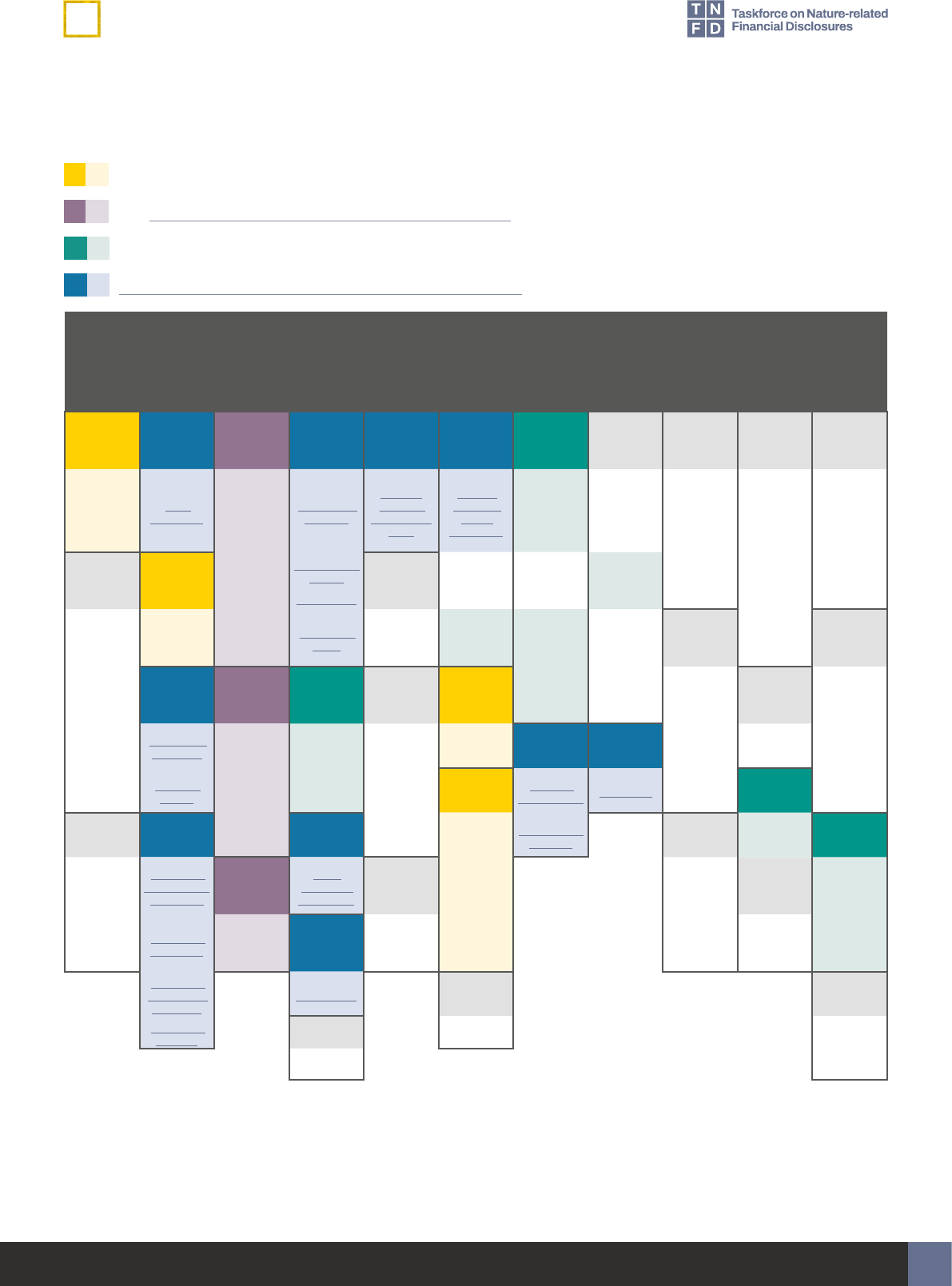

The TNFD’s metrics approach includes dierent

categories of metrics (Figure 1). These include:

• A small set of core metrics – ‘core global metrics’ that

apply to all sectors and ‘core sector metrics’ for each

sector – to be disclosed on a comply or explain basis;

and

• A larger set of additional metrics, which are

recommended for disclosure, where relevant, to best

represent an organisation’s material nature-related

issues, based on their specic circumstances.

Sector-specic metrics form an important part of this

approach. This reects the diversity of business models

across value chains and their interface with nature

across and within sectors. Sector-specic metrics

help nancial institutions to compare organisations

within the same sector, which often face similar nature-

relatedissues.

3

Draft sector metrics

For market consultation and feedback – December 2023

For the sectors shown in Figure 2, this discussion

paperpresents:

• Proposed guidance on how to apply the TNFD core

global disclosure metrics in each sector, where

relevant;

• Proposed core sector disclosure metrics:

Organisations in these sectors would be expected to

disclose these metrics on a comply or explain basis

once they are nalised in 2024 and incorporated into

TNFD additional guidance; and

• Proposed additional sector disclosure metrics:

Metrics that an organisation may use, where relevant,

to best represent its material nature-related issues,

based on its specic circumstances.

The proposed metrics and guidance have been

developed in consultation with key stakeholders,

including market participants, industry associations and

knowledge partners. They have been structured around

SASB’s Sustainable Industry Classication System and

draw on sector metrics previously developed by GRI,

SASB and others.

Through this discussion paper, the TNFD aims to

gather feedback on this guidance and metrics in order

to assist organisations in specic sectors to make

disclosures in line with the TNFD Recommendations.

Proposed disclosure metrics for nancial institutions

are detailed separately in the Additional Guidance for

Financial Institutions, as part of guidance on the nancial

institution-specic context for the recommended

disclosures.

This document is a revision of the discussion paper

on sector metrics published in September 2023. The

proposed metrics for most of the sectors covered in

that document are now available in the respective draft

sector guidance documents. The proposed metrics for

the remaining sectors are presented here for market

consultation and feedback.

Figure 1: The TNFD metrics architecture

Core sector metrics

Strongly recommended

Comply or explain, once final

Sector guidance

Metrics issued in draft

for consultation

Annex 1

Core global metrics

Comply or explain

Dependencies

and impacts

Risks and

opportunities

GRAPHICS CODE: RDB

2

Additional metrics

Recommended for

disclosure, where relevant,

to best represent an

organisation’s material

nature-related issues,

based on their specific

circumstances

3

1

TNFD

Recommendations

TNFD

Recommendations

Annex 2

Relevant sector guidance,

once published

Food

Apparel & textiles

Construction

materials

4

Draft sector metrics

For market consultation and feedback – December 2023

Open for consultation

The TNFD welcomes feedback from market participants

and other stakeholders on the proposed approach to

sector metrics outlined in this discussion paper and in

the Additional Guidance for Financial Institutions. The

Taskforce will continue its open innovation approach to

nalise its sector metrics and sector guidance, which will

include TNFD Forum member briengs and consultation

workshops. Details on consultation activities will be

shared with Forum members and on the TNFD website.

Comments can be provided to the Taskforce through its

website until Friday 29 March 2024.

Box 1: Feedback questions on sector

metrics

The Taskforce welcomes feedback on the following

questions:

• How can the draft guidance to support

application of the core global metrics in each

sector be improved, in line with the principles

above? Is any further additional guidance

required? What should it cover?

• Are the proposed core sector metrics meaningful

and decision-useful for report users?

• Are the proposed core sector metrics

proportionate, reecting the capacity and cost

constraints of report preparers?

• What other sector metrics should be considered

by the Taskforce? Should they be core or

additional?

• What other, if any, positive impact metrics and

opportunity metrics are relevant in eachsector?

• What data and assurance issues or challenges

should the Taskforce consider in relation to the

metrics proposed?

Further questions at an individual sector level

are provided at the start of some sections of this

document.

The Taskforce plans to expand its coverage to other

sectors that have been identied as having signicant

dependencies and impacts on nature (Figure 2).

Organisations in sectors not yet covered can seek

guidance from industry best practice and guidance from

organisations such as GRI or SASB.

Further details on the TNFD metrics architecture and the

core global disclosure metrics can be found in Section 4

and Annex 1 of the TNFD Recommendations.

5

Draft sector metrics

For market consultation and feedback – December 2023

Figure 2: Coverage of the TNFD sector guidance, based on SASB’s SICS classication

Sectors with proposed metrics in this discussion paper

See TNFD Additional Guidance for Financial Institutions

Other TNFD priority sectors

Draft metrics published in additional draft sector guidance

Consumer goods

Extractives &

minerals

processing

Financials

Food &

beverage

Health care

Infrastructure

Renewable

resources &

alternative

energy

Resource

transformation

Services

Technology &

communications

Transportation

Apparel &

textiles

Coal

Capital

markets

Food

Biotech-

nology &

pharmaceu-

ticals

Utilities

Alternative

energy

Industrials Media Technology

Air trans-

portation

Apparel,

accessories

& footwear

Coal

operations

Asset man-

agement

& custody

activities

Agricultural

products

Biotech-

nology &

pharmaceu-

ticals

Electric

utilities &

power

generators

Biofuels

Aerospace &

defence

Advertising

& marketing

Electronic

manufactur-

ing services

& original

design man-

ufacturing

Airlines

Consumer

discre-

tionary

products

Construc-

tion mate-

rials

Investment

banking &

brokerage

Meat, poultry

& dairy

Aquaculture

Health care

retail

Gas utilities

& distributors

Fuel cells

& industrial

batteries

Containers &

packaging

Media &

entertain-

ment

Hardware

Air freight &

logistics

Appliance

manufac-

turing

Construction

materials

Security &

commodity

exchanges

Processed

foods

Drug

retailers

Water utilities

& services

Solar

technology

& project

developers

Electrical &

electronic

equipment

Hospitality

& recreation

Software &

IT services

Automo-

biles

Building

products &

furnishings

Metals &

mining

Corporate

& retail

banking

Beverages

Health care

providers

Infrastruc-

ture

Wind

technology

& project

developers

Industrial

machinery &

goods

Casinos &

gaming

Internet

media &

services

Automobiles

Household

& personal

products

Iron & steel

producers

Commercial

banks

Alcoholic

beverages

Health care

delivery

Engineering

& construc-

tion services

Forestry &

paper

Chemicals

Hotels &

lodging

Internet

media &

services

Auto parts

Toys &

sporting

goods

Metals &

mining

Consumer

nance

Non-

alcoholic

beverages

Health care

distributors

Real estate

Forestry

management

Chemicals

Leisure

facilities

Semicon-

ductors

Car rental &

leasing

Consumer

goods retail

Oil & gas

Mortgage

nance

Food &

beverage

retail

Managed

care

Home

builders

Pulp & paper

products

Consumer

services

Semicon-

ductors

Marine

transporta-

tion

Multiline and

speciality

retailers &

distributors

Oil & gas –

exploration &

production

Insurance

Food

retailers &

distributors

Medical

technology

Real estate Education

Telecommu-

nications

Cruise lines

E-commerce

Oil & gas –

midstream

Insurance Restaurants

Medical

equipment &

supplies

Real estate

services

Professional

&

commercial

services

Telecom-

munication

services

Marine trans-

portation

Oil & gas –

rening and

marketing

Restaurants

Waste man-

agement

Land trans-

portation

Oil & gas –

services

Tobacco

Waste

management

Rail trans-

portation

Tobacco

Road trans-

portation

Draft sector metrics

For market consultation and feedback – December 2023

6

Consumer goods

Apparel & textiles

The value chain components for Apparel & textiles

are categorised by tier. Tier 0 corresponds to direct

operations, and Tiers 1-4 correspond to dierent levels

of upstream components. For tiering denitions, see

World Research Institute (2021) Roadmap to Net Zero:

Delivering Science-Based Targets in the Apparel Sector.

Organisations should refer to Annex 1 of the TNFD

Recommendations for further information on the core

global disclosure metrics.

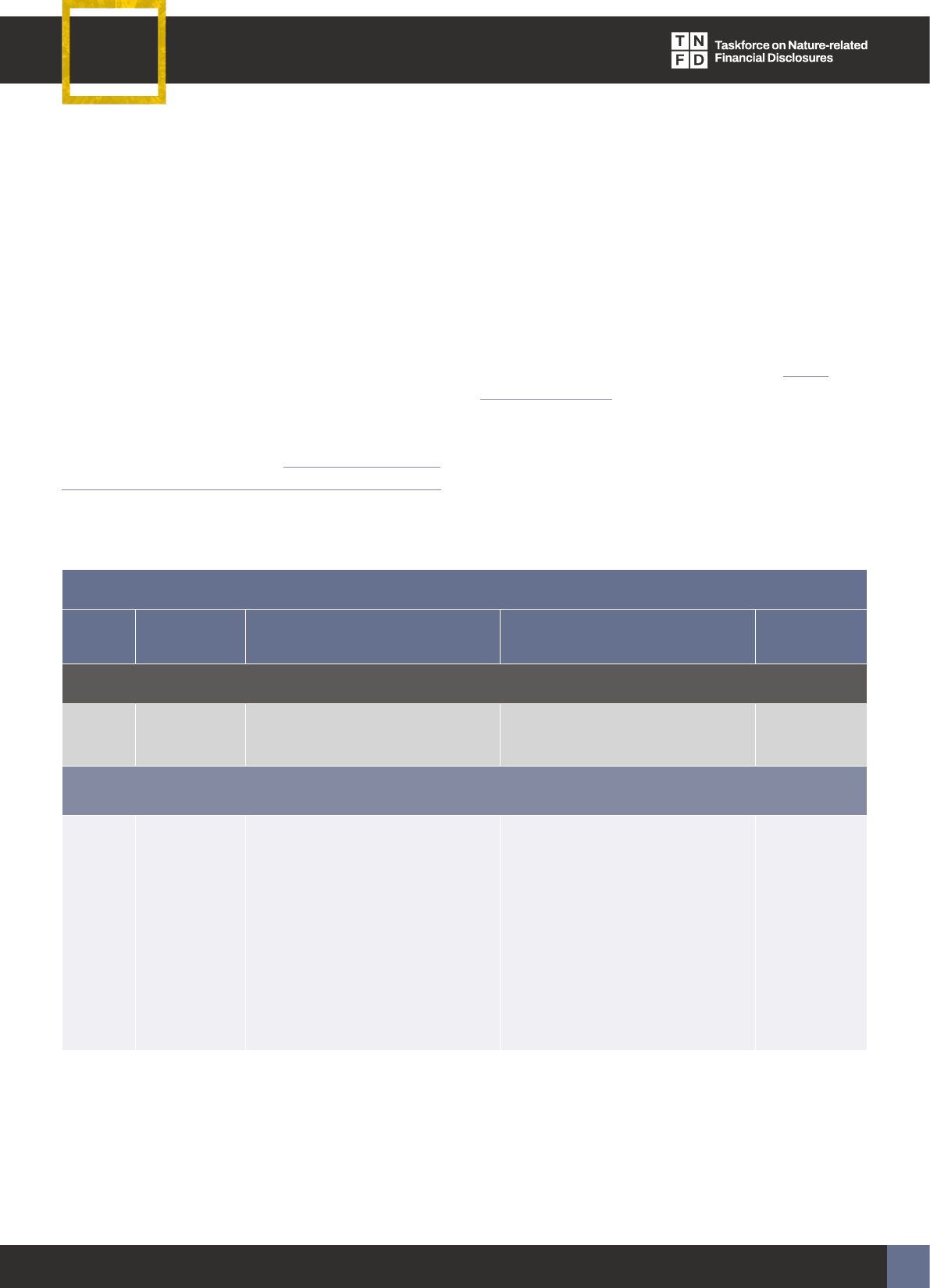

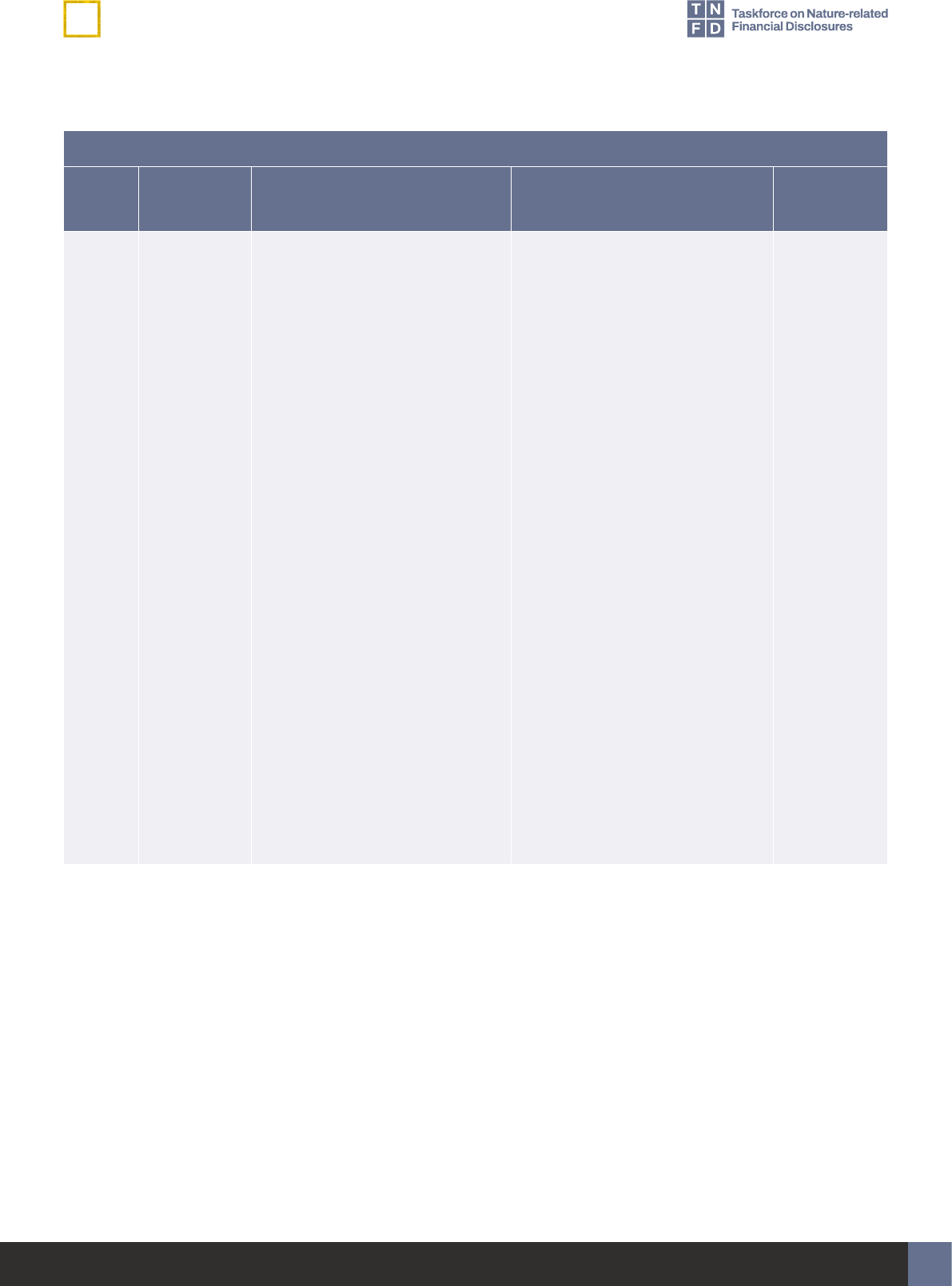

Proposed guidance on the application of the core global disclosure metrics

Apparel & textiles

Metric

no.

Core global

indicator

Core global metric

Proposed guidance for

thissector

Source

Driver of nature change: Climate change

GHG

emissions

Refer to IFRS S2 Climate-related

Disclosure Standard.

No further guidance.

Driver of nature change: Land/freshwater/ocean-use change

C1.0 Total spatial

footprint

Total spatial footprint (km

2

) (sum

of):

• Total surface area controlled/

managed by the organisation,

where the organisation has

control(km

2

);

• Total disturbed area (km

2

);and

• Total rehabilitated/restored area

(km

2

).

No further guidance.

7

Draft sector metrics

For market consultation and feedback – December 2023

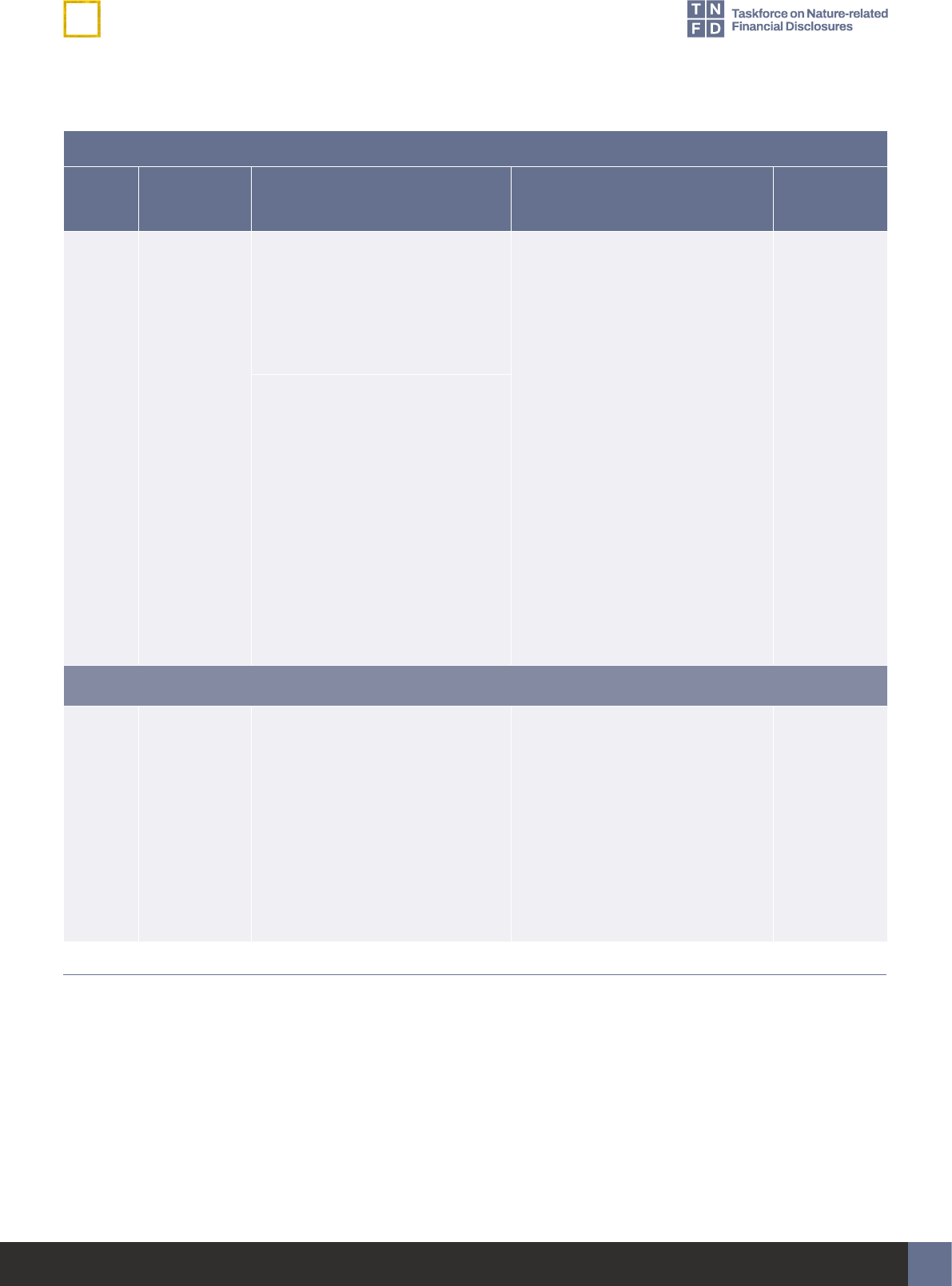

Apparel & textiles

Metric

no.

Core global

indicator

Core global metric

Proposed guidance for

thissector

Source

C1.1 Extent

of land/

freshwater/

ocean-use

change

Extent of land/freshwater/ocean

ecosystem use change (km

2

) by:

• Type of ecosystem;

3

and

• Type of business activity.

Tier 4, Upstream

Land-use change to report under

the core global disclosure metric

should include:

• Agriculture-driven terrestrial

natural ecosystem conversion

since 2020,

4

including, at least,

conversion of primary forests,

other naturally regenerating

(second-growth) forests and

freshwater natural ecosystems,

linked to land owned, leased

operated, nanced or

sourcedfrom.

Refer to

Food and

agriculture

metrics

Extent of land/freshwater/ocean

ecosystem conserved or restored

(km

2

), split into:

• Voluntary; and

• Required by statutes or

regulations.

Tier 4, Upstream

The extent conserved or restored

under the core global disclosure

metric should include:

• Area reforested in direct

operations or in the supply

chain of the corporation; and

• Area of wetlands rewetted in

direct operations or supply

chain of the corporation.

Refer to

Food and

agriculture

metrics

Extent of land/freshwater/ocean

ecosystem that is sustainably

managed (km

2

)by:

• Type of ecosystem;

5

and

• Type of business activity.

No further guidance.

3 When disclosing on ecosystem types, refer to the International Union for Conservation of Nature Global Ecosystem Typology.

4 Or other regional or sectoral cuto dates.

5 When disclosing on ecosystem types, refer to the International Union for Conservation of Nature Global Ecosystem Typology.

8

Draft sector metrics

For market consultation and feedback – December 2023

Apparel & textiles

Metric

no.

Core global

indicator

Core global metric

Proposed guidance for

thissector

Source

Driver of nature change: Pollution/pollution removal

C2.0 Pollutants

released to

soil split by

type

Pollutants released to soil

(tonnes) by type, referring to

sector-specic guidance on types

of pollutants

Tier 4, Upstream

Pollutants to report under the core

global disclosure metric should

include:

• Pesticides used by toxicity

hazard level (either extremely

hazardous, highly hazardous,

moderately hazardous,

slightly hazardous, or unlikely

to present an acute hazard)

against baseline.

• Nitrogen balance:

• Nitrogen input from livestock

manure and fertilisers; and

• Nitrogen output.

• Phosphorus balance:

• Phosphorus input; and

• Phosphorus output.

6

• If relevant, balances for

potassium and other nutrients

(e.g. micronutrients).

Refer to

Food and

agriculture

metrics

6 To calculate the nutrient balance minus nutrient inputs with outputs. A negative value indicates risk of soil fertility degradation and a positive

value signals pollution risk.

9

Draft sector metrics

For market consultation and feedback – December 2023

Apparel & textiles

Metric

no.

Core global

indicator

Core global metric

Proposed guidance for

thissector

Source

C2.1 Wastewater

discharged

Volume of water discharged (m

3

),

split into:

• Total;

• Freshwater; and

• Other.

7

Including:

• Concentrations of key

pollutants in the wastewater

discharged, by type of pollutant,

referring to sector-specic

guidance for types of pollutants;

and

• Temperature of water

discharged, where relevant.

Tier 0, Direct operations

Pollutants to report under the core

global disclosure metric should

include:

• Nutrients (nitrogen and

phosphorus);

• Pesticides;

• Organic loading (including crop

and livestock excreta);

• Allergenic dyes;

• Pathogens;

• Metals; and

• Other and emerging pollutants

(including antimicrobials and

other veterinary medicines).

Adapted

from TNFD

Food and

agriculture

metrics,

FAIRR Index,

FAO (2017)

7 Freshwater: (≤1,000 mg/L Total Dissolved Solids). Other: (>1,000 mg/L Total Dissolved Solids). Reference: GRI (2018) GRI 303-4 Water

discharge.

10

Draft sector metrics

For market consultation and feedback – December 2023

Apparel & textiles

Metric

no.

Core global

indicator

Core global metric

Proposed guidance for

thissector

Source

C2.2 Waste

generation

and disposal

Weight of hazardous and non-

hazardous waste generated by

type (tonnes), referring to sector-

specic guidance for types of

waste.

Weight of hazardous and non-

hazardous waste (tonnes)

disposed of, split into:

• Waste incinerated (with and

without energy recovery);

• Waste sent to landll; and

• Other disposal methods.

Weight of hazardous and non-

hazardous waste (tonnes) diverted

from landll, split into waste:

• Reused;

• Recycled; and

• Other recovery operations.

Tier 0, Direct operations

In reporting the core global

disclosure metric, an organisation

should include:

• Weight and percentage

of apparel products and

fabric waste by type in the

company’s direct operations,

disaggregated by destination

(e.g. landll or incineration).

In reporting the core global

disclosure metric, an organisation

should:

• Refer to the Sustainable

Apparel Coalition’s Higg

Facility Environmental Module

(FEM) for types of production

hazardous waste (e.g. empty

chemical drums and containers,

expired/used/unused

chemicals).

Sustainable

Apparel

Coalition

(2022)

C2.3 Plastic

pollution

Plastic footprint as measured by

total weight (tonnes) of plastics

(polymers, durable goods and

packaging) used or sold broken

down into the raw material

content.

8

For plastic packaging, percentage

of plastics that is:

• Re-usable;

• Compostable;

• Technically recyclable; and

• Recyclable in practice and at

scale.

Tier 0, Direct operations

In reporting the core global

disclosure metric, an organisation

should include:

• Total weight of plastic

material (primary, secondary

and tertiary) used for textile

products.

TNFD

8 Raw material content: % of virgin fossil-fuel feedstock; % of post-consumer recycled feedstock; % of post-industrial recycled feedstock; % of virgin

renewable feedstock.

11

Draft sector metrics

For market consultation and feedback – December 2023

Apparel & textiles

Metric

no.

Core global

indicator

Core global metric

Proposed guidance for

thissector

Source

C2.4 Non-GHG air

pollutants

Non-GHG air pollutants (tonnes)

by type:

• Particulate matter (PM

2.5

and/

or PM

10

);

• Nitrogen oxides (NO

2

, NO and

NO

3

);

• Volatile organic compounds

(VOC or NMVOC);

• Sulphur oxides (SO

2

, SO, SO

3

,

SO

X

); and

• Ammonia (NH

3

).

Tier 0, Direct operations

In determining additional

pollutants to report under the

core global disclosure metric, an

organisation should refer to the

Sustainable Apparel Coalition’s

Higg Facility Environmental

Module (FEM)’s Air Emissions

2022.

SASB and

Sustainable

Apparel

Coalition

(2022)

Driver of nature change: Resource use/replenishment

C3.0 Water

withdrawal

and

consumption

from areas

of water

scarcity

Water withdrawal and

consumption

9

(m

3

) from areas

of water scarcity, including

identication of water source.

10

No further guidance.

C3.1 Quantity of

high-risk

natural

commodities

sourced from

land/ocean/

freshwater

Quantity of high-risk natural

commodities

11

(tonnes) sourced

from land/ocean/freshwater, split

into types, including proportion of

total natural commodities.

No further guidance.

9 Water consumption is equal to water withdrawal less water discharge. Reference: GRI (2018) GRI 303-5.

10 Surface water; groundwater; seawater; produced water; third-party water. Reference: GRI (2018) GRI 303-3.

11 Users should refer to the Science Based Targets Network (SBTN) High Impact Commodity List (HICL) and indicate what proportion of these

commodities represent threatened and CITES listed species.

12

Draft sector metrics

For market consultation and feedback – December 2023

Apparel & textiles

Metric

no.

Core global

indicator

Core global metric

Proposed guidance for

thissector

Source

C3.1 Quantity of

high-risk

natural

commodities

sourced from

land/ocean/

freshwater

Quantity of high-risk natural

commodities

12

(tonnes) sourced

under a sustainable management

plan or certication programme,

including proportion of total high-

risk natural commodities.

Tier 4, Upstream

In reporting the core global

disclosure metric, an organisation

should include:

• Natural bre or raw material

products on the SBTN High

Impact Commodity List (i.e.

cotton, leather, wool) certied

to a relevant third-party

environmental, social, and/or

animal welfare standard such as

Textile Exchange’s Responsible

Wool Standard (RWS),

Responsible Down Standard

(RDS), Responsible Mohair

Standard (RMS), or Responsible

Alpaca Standard (RAS).

The organisation should specify

which certication applies and the

percentages of certied bres or

raw materials by category.

Adapted from

SASB textile

Driver of nature change: Invasive alien species and other

C4.0 Placeholder

indicator:

Measures

against

unintentional

introduction

of invasive

alien species

(IAS)

13

Proportion of high-risk activities

operated under appropriate

measures to prevent unintentional

introduction of IAS, or low-risk

designed activities.

No further guidance.

12 Users should refer to the Science Based Targets Network (SBTN) High Impact Commodity List (HICL) and indicate what proportion of these

commodities represent threatened and CITES listed species.

13 Due to the measurement of levels of invasive species for organisations being a developing area, the chosen indicator focuses on whether an

appropriate management response is in place for the organisation. The additional sets of metrics contain measurement of the level of invasive

species within an area. The TNFD intends to do further work with experts to dene ‘high-risk activities’ and ‘low-risk designed activities’.

13

Draft sector metrics

For market consultation and feedback – December 2023

Apparel & textiles

Metric

no.

Core global

indicator

Core global metric

Proposed guidance for

thissector

Source

State of nature

C5.0 Placeholder

indicator:

Ecosystem

condition

For those organisations that

choose to report on state of nature

metrics, the TNFD encourages

them to report the following

indicators, and to refer to the

TNFD additional guidance on

measurement of the state of

nature in Annex 2 of the LEAP

approach:

• Level of ecosystem condition

by type of ecosystem and

business activity;

• Impacts on mean species

extinction risk.

There are a number of dierent

measurement options for these

indicators. The TNFD does not

currently specify one metric as

there is no single metric that will

capture all relevant dimensions of

changes to the state of nature and

a consensus is still developing.

The TNFD will continue to work

with knowledge partners to

increase alignment.

No further guidance.

Placeholder

indicator:

Species

extinction

risk

No further guidance.

14

Draft sector metrics

For market consultation and feedback – December 2023

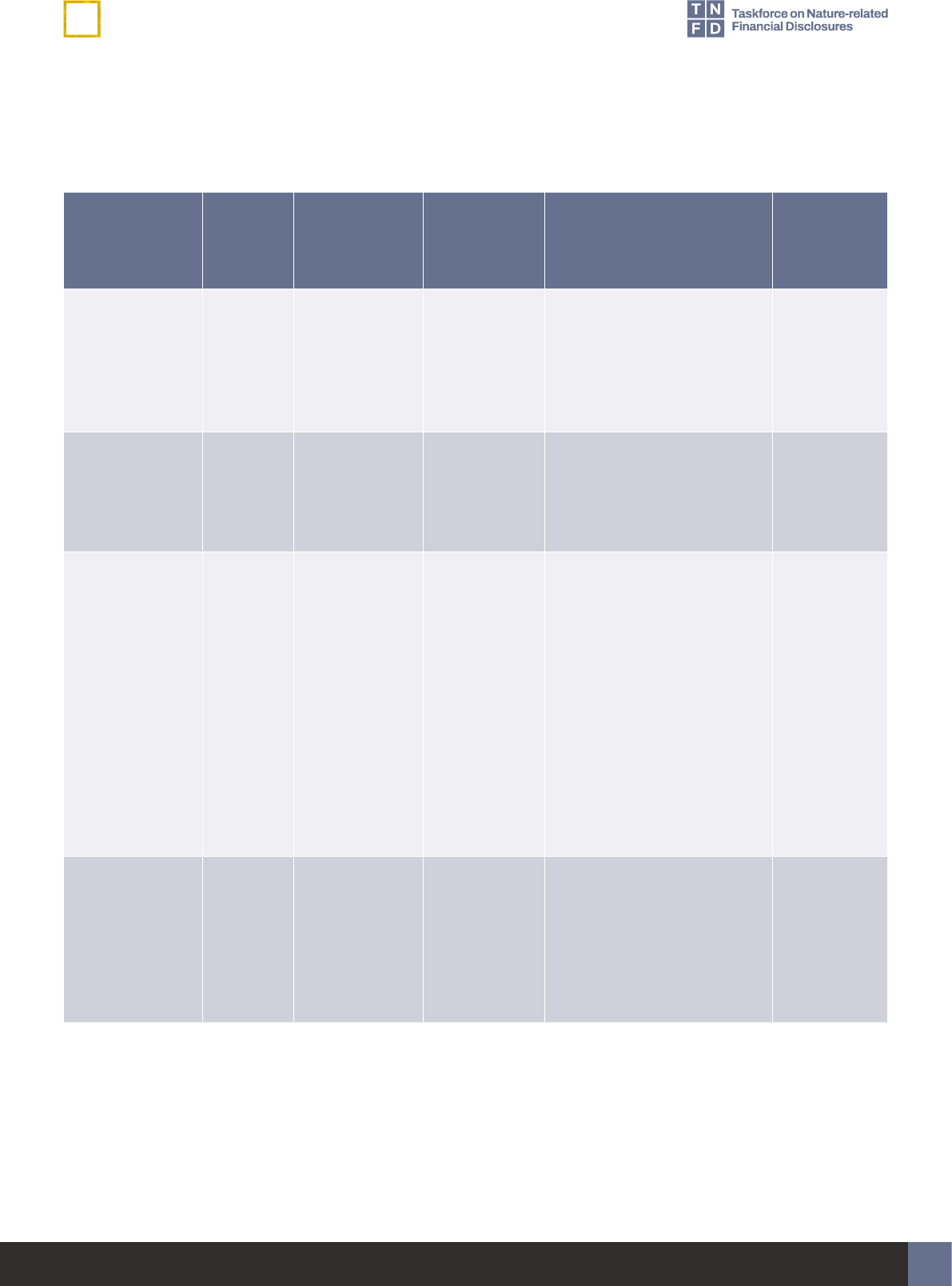

Proposed core sector disclosure indicators and metrics – Apparel & textiles

Metric

category

Metric

subcategory

Indicator Proposed core sector disclosure

indicator or metric

Source

Impact driver Land/freshwater/

ocean-use change

Extent of land/

freshwater/

ocean-use

change

Tier 4, Upstream

Percentage of production volume

from land owned, leased, managed

or sourced from determined to be

deforestation-free, by product.

Refer to

Food and

agriculture

metrics

Tier 4, Upstream

Percentage of land managed or sourced

from that deploys practices with

measurable regenerative or sustainable

outcomes. An organisation should

describe and disclose the denition of

regenerative or sustainable agriculture

used for disclosure.

14

Refer to

Food and

agriculture

metrics

Management of

chemicals

Tier 0–4, Upstream and direct

operations

Percentage of chemical products used

in facilities that are certied by the Zero

Discharge of Hazardous Chemicals

Manufacturing Restricted Substances

List (ZDHC MRSL) or equivalent

relevant program such as 4S CHEM

(CHEM 4sustainability protocol).

Adapted from

SASB

CG-AA-

250a.1

Resource use/

replenishment

Quantity of

high-risk natural

commodities

sourced from

land/ocean/

freshwater

Tier 4, Upstream

Percentage of natural bre or raw

material products produced or sourced

from regions with high or extremely high

baseline water stress.

Adapted from

SASB textile

14 The measures start when a baseline has been undertaken for the corporation to track regeneration of environmental assets against, as

disclosure data for the metric.

15

Draft sector metrics

For market consultation and feedback – December 2023

Proposed additional sector disclosure indicators and metrics – Apparel & textiles

Metric category Metric

subcategory

Indicator Proposed additional sector

disclosure indicator or metric

Source

Impact driver Pollution/pollution

removal

Waste Percentage of unsold apparel

products in all selling points that

are recycled or given away (%).

TNFD

Plastic pollution Total weight of plastics (tonnes)

commonly classied as

problematic (PS, PVC, EPC,

multilayer plastic packaging,

undetectable carbon black).

TNFD

Response Dependency,

impact, risk and

opportunity

management

Dependency,

impact, risk and

opportunity

assessment

Company’s bre and raw material

product composition (tonnes) and

the share (%) of priority material

(e.g. cotton, leather, wool,

polyester), indicating whether

each is from recycled sources.

Textile

Exchange

Corporate

Benchmark

Voluntary

conservation,

restoration and

regeneration

Area (km

2

) of land used (for

agriculture, grazing and/

or forestry) that employs

regenerative practices with

measurable regenerative

outcomes, referencing the

denition used (e.g. from OP2B or

Textile Exchange).

Related to

GBF target 10

State of nature Ecosystem extent

and condition

Ecosystem

condition

Concentration of key pollutants

around key water basins in which

the company is operating, by

type (m

3

or equivalent): nutrients

(nitrogen and phosphorus levels),

pesticides, organic loading

(including crop and livestock

excreta), pathogens, metals,

other and emerging pollutants

(including antibiotics and other

veterinarymedicines).

Adapted from

FAIRR (2022),

FAO (2017)

Draft sector metrics

For market consultation and feedback – December 2023

16

Extractives & minerals processing

Construction materials

The TNFD recognises the important contributions from

this sector to habitat fragmentation and noise pollution.

The TNFD encourages organisations to measure these

impact drivers and would welcome feedback on industry

best practices. In particular:

• How can metrics like the Singapore Index be applied

in a corporate reporting context in this sector?

• How do organisations in this sector currently measure

noise pollution? At what times of day? Is pitch

alsomonitored?

• What noise metrics would be most appropriate to

understand the impact of human noise generation

onnature?

Organisations should refer to Annex 1 of the TNFD

Recommendations for further information on the core

global disclosure metrics.

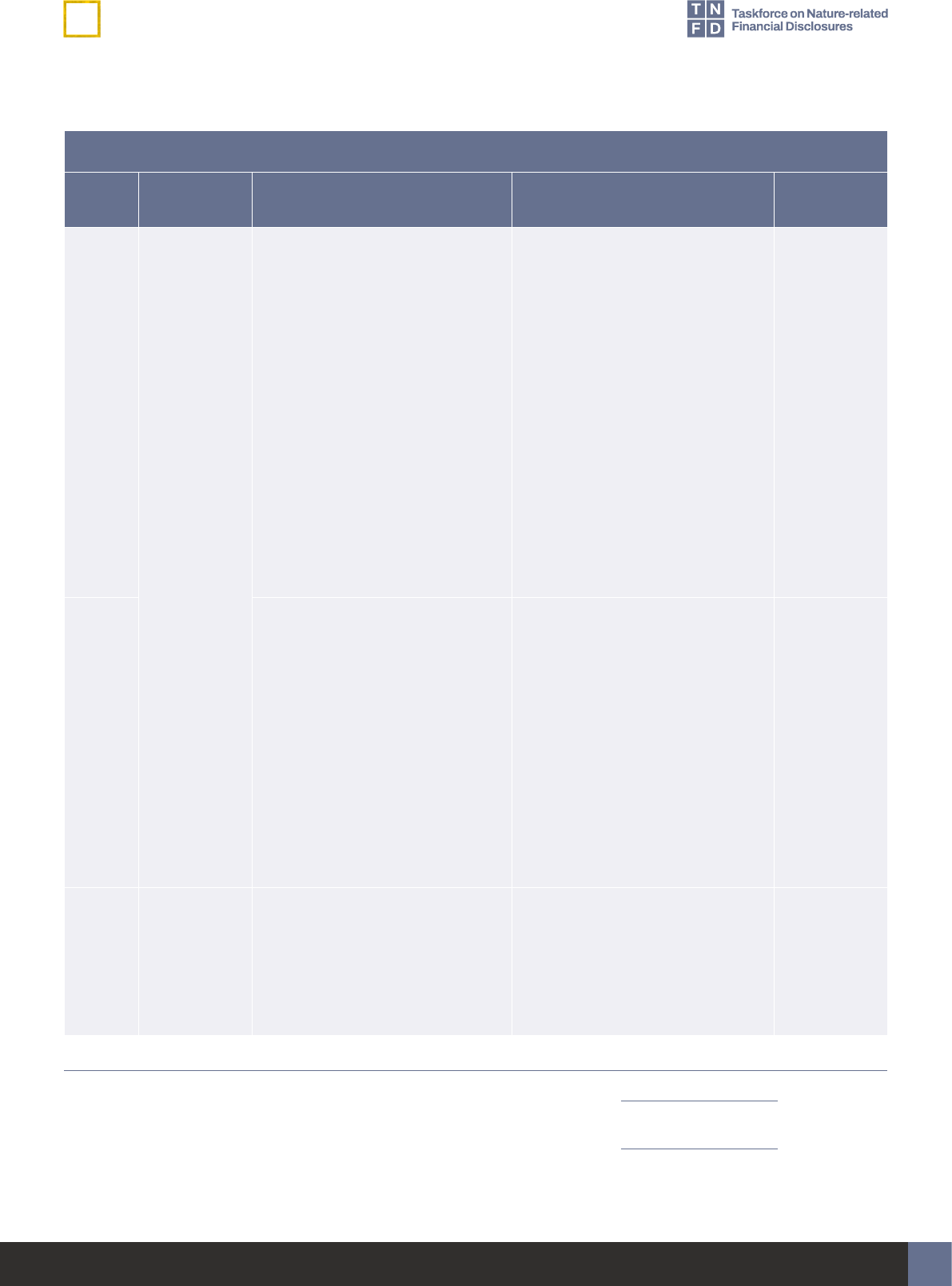

Proposed guidance on the application of the core global disclosure metrics

Construction materials

Metric

no.

Core global

indicator

Core global metric

Proposed guidance for

thissector

Source

Driver of nature change: Climate change

GHG

emissions

Refer to IFRS S2 Climate-related

Disclosure Standard.

No further guidance.

Driver of nature change: Land/freshwater/ocean-use change

C1.0 Total spatial

footprint

Total spatial footprint (km

2

) (sum

of):

• Total surface area controlled/

managed by the organisation,

where the organisation has

control (km

2

);

• Total disturbed area (km

2

); and

• Total rehabilitated/restored area

(km

2

).

The land footprint under the core

global disclosure metric should

include land owned, leased or

managed in the exploration,

development and production, or

quarry/mine closure, and post-

closure project phases.

GRI 304-1

17

Draft sector metrics

For market consultation and feedback – December 2023

Construction materials

Metric

no.

Core global

indicator

Core global metric

Proposed guidance for

thissector

Source

C1.1 Extent

of land/

freshwater/

ocean-use

change

Extent of land/freshwater/ocean

ecosystem use change (km

2

) by:

• Type of ecosystem;

15

and

• Type of business activity.

In reporting the core global

disclosure metric, land-use

change should cover the gross

area disturbed in the reporting

period. This includes land in

the exploration, development

and production, or quarry/mine

closure, and post-closure project

phases.

SASB (2019)

EM-CM-

160a.2; GRI

304-3

Extent of land/freshwater/ocean

ecosystem conserved or restored

(km

2

), split into:

• Voluntary; and

• Required by statutes or

regulations.

The extent conserved or restored

reported under the core global

disclosure metric should include

only activity within the value chain.

TNFD

Extent of land/freshwater/ocean

ecosystem that is sustainably

managed (km

2

) by:

• Type of ecosystem;

16

and

• Type of business activity.

No further guidance.

15 When disclosing on ecosystem types, refer to the International Union for Conservation of Nature Global Ecosystem Typology.

16 When disclosing on ecosystem types, refer to the International Union for Conservation of Nature Global Ecosystem Typology.

18

Draft sector metrics

For market consultation and feedback – December 2023

Construction materials

Metric

no.

Core global

indicator

Core global metric

Proposed guidance for

thissector

Source

Driver of nature change: Pollution/pollution removal

C2.0 Pollutants

released to

soil split by

type

Pollutants released to soil

(tonnes) by type, referring to

sector-specic guidance on types

of pollutants.

No further guidance. TNFD

C2.1 Wastewater

discharged

Volume of water discharged (m

3

),

split into:

• Total;

• Freshwater; and

• Other.

17

Including:

• Concentrations of key

pollutants in the wastewater

discharged, by type of pollutant,

referring to sector-specic

guidance for types of pollutants;

and

• Temperature of water

discharged, where relevant.

Reporting of water discharged

under the core global disclosure

metric should additionally be

broken down by destination:

• Surface water;

• Groundwater;

• Seawater; and

• Third-party water, and the

volume of this total sent for use

to other organisations.

Pollutants and water quality

metrics to report under the core

global disclosure metric include:

• pH;

• TSS (Total Suspended Solids);

• TDS (Total Dissolved Solids);

• Mercury;

• TPH (Total Petroleum

Hydrocarbons);

• BOD (Biochemical Oxygen

Demand);

• Dissolved solids; and

• Suspended solids.

GRI 303-4;

ENCORE

17 Freshwater: (≤1,000 mg/L Total Dissolved Solids). Other: (>1,000 mg/L Total Dissolved Solids). Reference: GRI (2018)

GRI 303-4 Water discharge.

19

Draft sector metrics

For market consultation and feedback – December 2023

Construction materials

Metric

no.

Core global

indicator

Core global metric

Proposed guidance for

thissector

Source

C2.2 Waste

generation

and disposal

Weight of hazardous and non-

hazardous waste generated by

type (tonnes), referring to sector-

specic guidance for types of

waste.

Weight of hazardous and non-

hazardous waste (tonnes)

disposed of, split into:

• Waste incinerated (with and

without energy recovery);

• Waste sent to landll; and

• Other disposal methods.

Weight of hazardous and non-

hazardous waste (tonnes)

diverted from landll, split into

waste:

• Reused;

• Recycled; and

• Other recovery operations.

Types of waste to report under

the core global disclosure metric

include:

• Slags, dusts, sludges, used oil,

other solid waste that meet the

TNFD denition of waste.

SASB (2018)

construction

materials:

EM-CM-

150a.1

GRI (2022)

GRI

Standards

Glossary

C2.3 Plastic

pollution

Plastic footprint as measured by

total weight (tonnes) of plastics

(polymers, durable goods and

packaging) used or sold broken

down into the raw material

content.

18

For plastic packaging, percentage

of plastics that is:

• Re-usable;

• Compostable;

• Technically recyclable; and

• Recyclable in practice and at

scale.

No further guidance.

18 Raw material content: % of virgin fossil-fuel feedstock; % of post-consumer recycled feedstock; % of post-industrial recycled feedstock; % of

virgin renewable feedstock.

20

Draft sector metrics

For market consultation and feedback – December 2023

Construction materials

Metric

no.

Core global

indicator

Core global metric

Proposed guidance for

thissector

Source

C2.4 Non-GHG air

pollutants

Non-GHG air pollutants (tonnes)

by type:

• Particulate matter (PM

2.5

and/

or PM

10

);

• Nitrogen oxides (NO

2

, NO and

NO

3

);

• Volatile organic compounds

(VOC or NMVOC);

• Sulphur oxides (SO

2

, SO, SO

3

,

SO

X

); and

• Ammonia (NH

3

).

Additional pollutants to report

under the core global disclosure

metric include:

• Carbon monoxide (CO);

• Dioxins/furans, including but

not limited to the sum of the 17

congeners of polychlorinated

dibenzodioxins (PCDDs) and

polychlorinated dibenzofurans

(PCDFs) that contain

chlorine;and

• Heavy metals (includes mercury

(Hg), cadmium (Cd), thallium

(Tl), antimony (Sb), arsenic

(As), lead (Pb), chromium

(Cr), cobalt (Co), copper (Cu),

manganese (Mn), nickel (Nl) and

vanadium(V).

TNFD

21

Draft sector metrics

For market consultation and feedback – December 2023

Construction materials

Metric

no.

Core global

indicator

Core global metric

Proposed guidance for

thissector

Source

Driver of nature change: Resource use/replenishment

C3.0 Water

withdrawal

and

consumption

from areas

of water

scarcity

Water withdrawal and

consumption

19

(m

3

) from areas

of water scarcity, including

identication of water source.

20

In reporting the core global

disclosure metric, an organisation

should include:

• Total freshwater (≤1000 mg/l

of Total Dissolved Solids)

withdrawal, including from

natural open sources such

as rivers, lakes, natural

ponds, streams, creeks; from

groundwater (wells, boreholes,

water below soil surface); from

municipal and/or from third

parties; from quarry dewatering

used in operations;

• Total non-freshwater (>1000

mg/l of Total Dissolved Solids)

withdrawal, including from

sources of high salinity or

pollutants; and

• Harvested rainwater: Volume

of precipitation (rainwater or

snowmelt) that is collected

onsite (e.g. settling ponds,

inactive quarry area that has not

yet reached the groundwater

table).

Water from quarry dewatering that

is not used should be reported

separately.

An organisation should dierentiate

withdrawal from groundwater

sources that are recharged and

non-recharged.

GCCA

(2019)

GRI-303-4

GRI-G4

Construction

& Real

Estate

Disclosures

EN8-EN9

SASB Real

Estate IF-

RE-140a.1.,

IF-RE-

140a.2., IF-

RE-140a.3.

Recharged

groundwater

from GRI, as

above

19 Water consumption is equal to water withdrawal less water discharge. Reference: GRI (2018) GRI 303-5.

20 Surface water; groundwater; seawater; produced water; third-party water. Reference: GRI (2018) GRI 303-3.

22

Draft sector metrics

For market consultation and feedback – December 2023

Construction materials

Metric

no.

Core global

indicator

Core global metric

Proposed guidance for

thissector

Source

C3.1 Quantity of

high-risk

natural

commodities

sourced from

land/ocean/

freshwater

Quantity of high-risk natural

commodities

21

(tonnes) sourced

from land/ocean/freshwater, split

into types, including proportion of

total natural commodities.

Commodities to report under

the core global disclosure metric

include: limestone chalk marl,

silica correctives, alumina and

ferrous, natural gypsum, pozzolan,

primary aggregates, sand, and

coal.

TNFD;

GRI-G4 Real

Estate &

Construction,

G4-EN1;

SBTN High

Impact

Commodity

list

Quantity of high-risk natural

commodities

22

(tonnes) sourced

under a sustainable management

plan or certication programme,

including proportion of total high-

risk natural commodities.

Driver of nature change: Invasive alien species and other

C4.0 Placeholder

indicator:

Measures

against

unintentional

introduction

of invasive

alien species

(IAS)

23

Proportion of high-risk activities

operated under appropriate

measures to prevent unintentional

introduction of IAS, or low-risk

designed activities.

No further guidance. TNFD;

GRI-G4 Real

Estate &

Construction,

G4-EN1;

SBTN High

Impact

Commodity

list

21 Users should refer to the Science Based Targets Network (SBTN) High Impact Commodity List (HICL) and indicate what proportion of these

commodities represent threatened and CITES listed species.

22 Users should refer to the Science Based Targets Network (SBTN) High Impact Commodity List (HICL) and indicate what proportion of these

commodities represent threatened and CITES listed species.

23 Due to the measurement of levels of invasive species for organisations being a developing area, the chosen indicator focuses on whether an

appropriate management response is in place for the organisation. The additional sets of metrics contain measurement of the level of invasive

species within an area. The TNFD intends to do further work with experts to dene ‘high-risk activities’ and ‘low-risk designed activities’.

23

Draft sector metrics

For market consultation and feedback – December 2023

Construction materials

Metric

no.

Core global

indicator

Core global metric

Proposed guidance for

thissector

Source

State of nature

C5.0 Placeholder

indicator:

Ecosystem

condition

For those organisations that

choose to report on state of nature

metrics, the TNFD encourages

them to report the following

indicators, and to refer to the

TNFD additional guidance on

measurement of the state of

nature in Annex 2 of the LEAP

approach:

• Level of ecosystem condition

by type of ecosystem and

business activity;

• Species extinction risk.

There are a number of dierent

measurement options for these

indicators. The TNFD does not

currently specify one metric as

there is no single metric that will

capture all relevant dimensions of

changes to the state of nature and

a consensus is still developing.

The TNFD will continue to work

with knowledge partners to

increase alignment.

No further guidance.

Placeholder

indicator:

Species

extinction

risk

24

Draft sector metrics

For market consultation and feedback – December 2023

Proposed core sector disclosure indicators and metrics – Construction materials

Metric category Metric subcategory Indicator Proposed core sector

disclosure indicator or metric

Source

Impact driver Pollution/pollution removal Spills Volume of spills of diesel, paints,

solvents and toxic chemicals

(m

3

), by national or company

spill classication scheme and

by type of ecosystem aected.

GRI 303-4;

ENCORE

25

Draft sector metrics

For market consultation and feedback – December 2023

Proposed additional sector disclosure indicators and metrics – Construction materials

Metric

category

Metric

subcategory

Indicator Proposed additional sector disclosure

indicator or metric

Source

Impact driver Pollution/

pollution removal

Disturbances Average light pollution levels, measured,

for example by:

• Night sky light pollution levels on the

Sky Quality Meter (SQM) Scale or Bortle

scale;

• Percentage of light xtures that fully cut-

o or fully shielded or below 60W; or

• Outdoor lighting (lumen/ha).

IUCN (2023)

Urban Nature

Indexes

Response Dependency,

impact, risk and

opportunity

management

General Proportion of materials used that are

recycled and reused input materials by

signicant categories of raw materials,

renewable materials and manufactured

products (%);

or

Share of total mass of materials, products

and components/systems for the new

build/refurbishment/t-out that have been

reused, repurposed or remanufactured,

either from the building undergoing

demolition, refurbishment, t-out or from

other buildings, third parties etc. (%).

GRI: G4-EN2

Percentage

of materials

used that are

recycled input

materials

UK Green

Building

Council

(2023)

Response Dependency,

impact, risk and

opportunity

management

General Total volume of water volume that has

been sustainably supplied, puried and/

or conserved in the same watershed

where the freshwater was withdrawn. This

includes volume of water from watershed

protection and restoration projects, from

water access and sanitation to community

projects and from water ecient agriculture

and water ecient irrigation practices.

TNFD

Draft sector metrics

For market consultation and feedback – December 2023

26

Infrastructure

Infrastructure; Real estate

The TNFD recognises the important contributions from

this sector to habitat fragmentation and noise pollution.

The TNFD encourages organisations to measure these

impact drivers and would welcome feedback on industry

best practices. In particular:

• How can metrics like the Singapore Index be applied

to a corporate reporting context in this sector?

• How do organisations in this sector currently measure

noise pollution? At what times of day? Is pitch also

monitored?

• What noise metrics would be most appropriate to

understand the impact of human noise generation on

nature?

Organisations should refer to Annex 1 of the TNFD

Recommendations for further information on the core

global disclosure metrics.

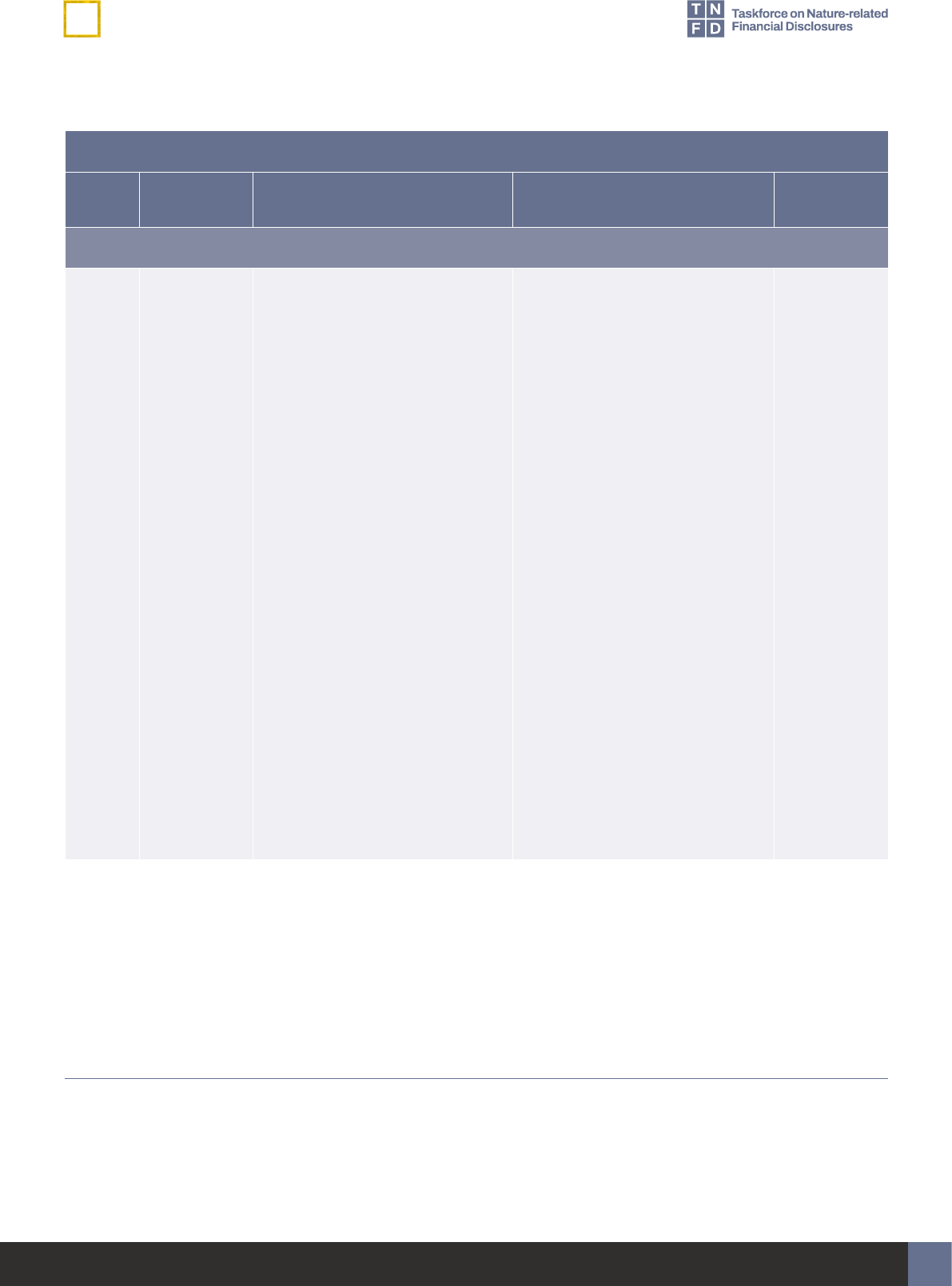

Proposed guidance on the application of the core global disclosure metrics

Engineering & construction services; Home builders; Real estate; Real estate services

Metric

no.

Core global

indicator

Core global metric Proposed guidance for

thissector

Source

Driver of nature change: Climate change

GHG

emissions

Refer to IFRS S2 Climate-related

Disclosure Standard.

No further guidance.

Driver of nature change: Land/freshwater/ocean-use change

C1.0 Total spatial

footprint

Total spatial footprint (km

2

)

(sumof):

• Total surface area controlled/

managed by the organisation,

where the organisation has

control (km

2

);

• Total disturbed area (km

2

); and

• Total rehabilitated/restored

area(km

2

).

Engineering & construction

services; Home builders; Real

estate; Real estate services

The land footprint under the core

global disclosure metric should

include land owned, leased or

managed.

GRI 304-1

27

Draft sector metrics

For market consultation and feedback – December 2023

Engineering & construction services; Home builders; Real estate; Real estate services

Metric

no.

Core global

indicator

Core global metric Proposed guidance for

thissector

Source

C1.1 Extent

of land/

freshwater/

ocean-use

change

Extent of land/freshwater/ocean

ecosystem use change (km

2

) by:

• Type of ecosystem;

24

and

• Type of business activity.

Engineering & construction

services; Home builders

Land-use change reported under

the core global disclosure metric

should distinguish land-use

changes by original land uses:

browneld sites, undeveloped

land, farmland, wetland etc.

Real estate; Real estate

services

No further guidance.

SASB (2019)

EM-CM-

160a.2; GRI

304-3

Land-use

change –

Adapted

from SITES

v2 Rating

System for

Sustainable

Land

Design and

Development

Extent of land/freshwater/ocean

ecosystem conserved or restored

(km

2

), split into:

• Voluntary; and

• Required by statutes or

regulations.

Engineering & construction

services; Home builders; Real

estate; Real estate services

The extent conserved or restored

under the core global disclosure

metric should include only activity

within the value chain.

TNFD

Extent of land/freshwater/ocean

ecosystem that is sustainably

managed (km

2

)by:

• Type of ecosystem;

25

and

• Type of business activity.

Engineering & construction

services; Home builders; Real

estate; Real estate services

No further guidance.

24 When disclosing on ecosystem types, refer to the International Union for Conservation of Nature Global Ecosystem Typology.

25 When disclosing on ecosystem types, refer to the International Union for Conservation of Nature Global Ecosystem Typology.

28

Draft sector metrics

For market consultation and feedback – December 2023

Engineering & construction services; Home builders; Real estate; Real estate services

Metric

no.

Core global

indicator

Core global metric Proposed guidance for

thissector

Source

Driver of nature change: Pollution/pollution remova

C2.0 Pollutants

released

to soil split

bytype

Pollutants released to soil

(tonnes) by type, referring to

sector-specic guidance on types

of pollutants

Engineering & construction

services; Home builders

No further guidance.

Real estate; Real estate

services

Pollutants to report under the core

global disclosure metric include:

• Volume of pesticides used by

toxicity hazard level (either

extremely hazardous, highly

hazardous, moderately

hazardous, slightly hazardous,

or unlikely to present an acute

hazard) against baseline;

• Chemical nitrogen fertilisers

input by source (tonnes of

nitrogen);

• Mineral phosphorus fertilisers

input by source (tonnes of

phosphorus); and

• Total manure and

compostinput.

TNFD; WHO

(2019)

29

Draft sector metrics

For market consultation and feedback – December 2023

Engineering & construction services; Home builders; Real estate; Real estate services

Metric

no.

Core global

indicator

Core global metric Proposed guidance for

thissector

Source

C2.1 Wastewater

discharged

Volume of water discharged (m

3

),

split into:

• Total;

• Freshwater; and

• Other.

26

Including:

• Concentrations of key

pollutants in the wastewater

discharged, by type of pollutant,

referring to sector-specic

guidance for types of pollutants;

and

• Temperature of water

discharged, where relevant.

Engineering & construction

services; Home builders

Reporting of water discharged

under the core global disclosure

metric should additionally be

broken down by destination:

• Surface water;

• Groundwater;

• Seawater; and

• Third-party water, and the

volume of this total sent for use

to other organisations.

Real estate; Real estate

services

Reporting of water discharged

under the core global disclosure

metric should additionally be

broken down by destination:

• Surface water;

• Groundwater;

• Seawater; and

• Third-party water, and the

volume of this total sent for use

to other organisations.

Pollutants to report under the core

global disclosure metric include:

• Dissolved solids; and

• Suspended solids.

GRI 303-4;

ENCORE

26 Freshwater: (≤1,000 mg/L Total Dissolved Solids). Other: (>1,000 mg/L Total Dissolved Solids). Reference: GRI (2018) GRI 303-4

Waterdischarge.

30

Draft sector metrics

For market consultation and feedback – December 2023

Engineering & construction services; Home builders; Real estate; Real estate services

Metric

no.

Core global

indicator

Core global metric Proposed guidance for

thissector

Source

C2.2 Waste

generation

and disposal

Weight of hazardous and non-

hazardous waste generated by

type (tonnes), referring to sector-

specic guidance for types of

waste.

Weight of hazardous and non-

hazardous waste (tonnes)

disposed of, splitinto:

• Waste incinerated (with and

without energy recovery);

• Waste sent to landll; and

• Other disposal methods.

Weight of hazardous and non-

hazardous waste (tonnes)

diverted from landll, split into

waste:

• Reused;

• Recycled; and

• Other recovery operations.

Engineering & construction

services; Home builders; Real

estate; Real estate services

Types of waste to report under

the core global disclosure metric

include:

• Slags, dusts, sludges, used oil,

other solid waste that meet the

TNFD denition of waste.

SASB (2018)

construction

materials:

EM-CM-

150a.1

GRI (2022)

GRI

Standards

Glossary

31

Draft sector metrics

For market consultation and feedback – December 2023

Engineering & construction services; Home builders; Real estate; Real estate services

Metric

no.

Core global

indicator

Core global metric Proposed guidance for

thissector

Source

C2.3 Plastic

pollution

Plastic footprint as measured by

total weight (tonnes) of plastics

(polymers, durable goods and

packaging) used or sold broken

down into the raw material

content.

27

For plastic packaging, percentage

of plastics thatis:

• Re-usable;

• Compostable;

• Technically recyclable; and

• Recyclable in practice and at

scale.

Engineering & construction

services; Home builders; Real

estate; Real estate services

No further guidance.

C2.4 Non-GHG air

pollutants

Non-GHG air pollutants (tonnes)

by type:

• Particulate matter (PM

2.5

and/

or PM

10

);

• Nitrogen oxides (NO

2

, NO and

NO

3

);

• Volatile organic compounds

(VOC or NMVOC);

• Sulphur oxides (SO

2

, SO, SO

3

,

SO

X

); and

• Ammonia (NH

3

).

Engineering & construction

services; Home builders; Real

estate; Real estate services

No further guidance.

27 Raw material content: % of virgin fossil-fuel feedstock; % of post-consumer recycled feedstock; % of post-industrial recycled feedstock; % of

virgin renewable feedstock.

32

Draft sector metrics

For market consultation and feedback – December 2023

Engineering & construction services; Home builders; Real estate; Real estate services

Metric

no.

Core global

indicator

Core global metric Proposed guidance for

thissector

Source

Driver of nature change: Resource use/replenishment

C3.0 Water

withdrawal

and

consumption

from areas

of water

scarcity

Water withdrawal and

consumption

28

(m

3

) from areas

of water scarcity, including

identication of water source.

29

Engineering & construction

services; Home builders

In reporting the core global metric,

an organisation should include:

• Known or metered water

withdrawal and consumption in

addition to listing non-metered

sources (e.g. seepage of

ground water in tunnels); and

• Water withdrawal from:

greywater, blackwater, treated

wastewater, desalination plants

and other water sources, as well

as total water withdrawal and

consumption.

This should cover all water

purchased and sourced but

may include itemisation of water

allocated to other parties as

the end user. The organisation

should dierentiate between water

withdrawal from groundwater

sources that are recharged and

non-recharged.

GRI-303-4

GRI-G4

Construction

& Real Estate

Disclosures

EN8-EN9

SASB Real

Estate IF-

RE-140a.1.,

IF-RE-

140a.2., IF-

RE-140a.3.

Recharged

groundwater

from GRI, as

above

28 Water consumption is equal to water withdrawal less water discharge. Reference: GRI (2018) GRI 303-5.

29 Surface water; groundwater; seawater; produced water; third-party water. Reference: GRI (2018) GRI 303-3.

33

Draft sector metrics

For market consultation and feedback – December 2023

Engineering & construction services; Home builders; Real estate; Real estate services

Metric

no.

Core global

indicator

Core global metric Proposed guidance for

thissector

Source

Real estate; Real estate

services

In reporting the core global metric,

an organisation should include:

• The share of total oor area for

which water withdrawal data

have been obtained;

• Water withdrawal by portfolio

area with data covered; and

• Water withdrawal from:

greywater, blackwater, treated

waste water, desalination plants

and other water sources, as well

as total water withdrawal and

consumption.

This should cover all water

purchased and sourced, but

may include itemisation of water

allocated to other parties as

the end user. The organisation

should dierentiate between water

withdrawal from groundwater

sources that are recharged and

non-recharged.

34

Draft sector metrics

For market consultation and feedback – December 2023

Engineering & construction services; Home builders; Real estate; Real estate services

Metric

no.

Core global

indicator

Core global metric Proposed guidance for

thissector

Source

C3.1 Quantity of

high-risk

natural

commodities

sourced from

land/ocean/

freshwater

Quantity of high-risk natural

commodities

30

(tonnes) sourced

from land/ocean/freshwater, split

into types, including proportion of

total natural commodities.

Engineering & construction

services; Home builders

Commodities to report under

the core global disclosure metric

include:

• Natural commodities:

aluminium, copper, gypsum,

iron, lead, sand and timber; and

• Manufactured commodities:

brick, cement, concrete, carpet,

glass, insulation products,

rubber and steel.

Real estate; Real estate

services

• No further guidance.

GRI-G4 Real

Estate &

Construction

G4-EN1,

SBTN High

Impact

Commodity

list

Quantity of high-risk natural

commodities

31

(tonnes) sourced

under a sustainable management

plan or certication programme,

including proportion of total high-

risk natural commodities.

Driver of nature change: Invasive alien species and other

C4.0 Placeholder

indicator:

Measures

against

unintentional

introduction

of invasive

alien species

(IAS)

32

Proportion of high-risk activities

operated under appropriate

measures to prevent unintentional

introduction of IAS, or low-risk

designed activities.

Engineering & construction

services; Home builders; Real

estate; Real estate services

No further guidance.

30 Users should refer to the Science Based Targets Network (SBTN) High Impact Commodity List (HICL) and indicate what proportion of these

commodities represent threatened and CITES listed species.

31 Users should refer to the Science Based Targets Network (SBTN) High Impact Commodity List (HICL) and indicate what proportion of these

commodities represent threatened and CITES listed species.

32 Due to the measurement of levels of invasive species for organisations being a developing area, the chosen indicator focuses on whether an

appropriate management response is in place for the organisation. The additional sets of metrics contain measurement of the level of invasive

species within an area. The TNFD intends to do further work with experts to dene ‘high-risk activities’ and ‘low-risk designed activities’.

35

Draft sector metrics

For market consultation and feedback – December 2023

Engineering & construction services; Home builders; Real estate; Real estate services

Metric

no.

Core global

indicator

Core global metric Proposed guidance for

thissector

Source

State of nature

C5.0 Placeholder

indicator:

Ecosystem

condition

For those organisations that

choose to report on state of nature

metrics, the TNFD encourages

them to report the following

indicators, and to refer to the

TNFD additional guidance on

measurement of the state of

nature in Annex 2 of the LEAP

approach:

• Level of ecosystem condition

by type of ecosystem and

business activity;

• Species extinction risk.

There are a number of dierent

measurement options for these

indicators. The TNFD does not

currently specify one metric as

there is no single metric that will

capture all relevant dimensions of

changes to the state of nature and

a consensus is still developing.

The TNFD will continue to work

with knowledge partners to

increase alignment.

Engineering & construction

services; Home builders; Real

estate; Real estate services

No further guidance.

Placeholder

indicator:

Species

extinction

risk

Engineering & construction

services; Home builders; Real

estate; Real estate services

No further guidance.

36

Draft sector metrics

For market consultation and feedback – December 2023

Proposed core sector disclosure indicators and metrics –

Engineering & construction services; Home builders; Real estate; Real estate services

Metric category Metric

subcategory

Indicator Proposed core sector disclosure

indicator or metric

Source

Impact driver Land/

freshwater/

ocean-use

change

Change to

connectivity

Engineering & construction services

Length (km) of linear infrastructure (e.g.

rail, road, fencing) built outside urban

areas by type, width (e.g. number of

lanes or tracks; metres) and surfacing.

TNFD

Impact driver Engineering & construction services

Number of fragmentation mitigation

measures (e.g. animal crossing points)

constructed for linear infrastructure

(count).

TNFD

Impact driver Pollution/

pollution

removal

Spills of

pollutants

Engineering & construction services;

Home builders

Volume of spills of diesel, paints,

solvents, and toxic chemicals

(m

3

), by national or company spill

classication scheme and by type of

ecosystemaected.

GRI 303-4;

ENCORE

Impact driver Resource use/

replenishment

Quantity

of high-

risk natural

commodities

sourced from

land/ocean/

freshwater

Engineering & construction services;

Home builders

Percentage of timber procured that is

from threatened species.

Based on

SITES v2

Rating

System for

Sustainable

Land

Design and

Development,

5.1

37

Draft sector metrics

For market consultation and feedback – December 2023

Proposed additional sector disclosure indicators and metrics –

Engineering & construction services; Home builders; Real estate; Real estate services

Sector Metric

category

Metric

subcategory

Indicator Proposed additional sector

disclosure indicator or

metric

Source

Engineering &

construction

services; Home

builders

Impact

driver

Land/

freshwater/

ocean-use

change

Land-use

change

Soil erosion on sites (m

3

),

measured as the average

change in soil depth,

multiplied by the area under

management.

TNFD

Engineering &

construction

services; Home

builders

Impact

driver

Land/

freshwater/

ocean-use

change

Land-use

change

Area of soil restored to a

minimum depth of 30.48cm

following disturbance by

construction activities (m

2

).

SITES Rating

system 7.3

and 7.4

Engineering &

construction

services; Home

builders; Real

estate; Real

estate services

Impact

driver

Pollution/

pollution

removal

Disturbances Average light pollution levels,

measured, for example, by:

• Night sky light pollution

levels on the Sky Quality

Meter (SQM) Scale or

Bortle scale;

• Percentage of light xtures

that fully cut-o or fully

shielded or below 60W; or

• Outdoor lighting

(lumen/ha).

IUCN (2023)

Urban Nature

Indexes

Engineering &

construction

services; Home

builders; Real

estate; Real

estate services

Impact

driver

Invasive

species and

other

Biological

alterations

Area of land owned,

controlled, managed or

leased cleared of invasive

species during reporting

period (km

2

).

TNFD

38

Draft sector metrics

For market consultation and feedback – December 2023

Sector Metric

category

Metric

subcategory

Indicator Proposed additional sector

disclosure indicator or

metric

Source

Engineering &

construction

services; Home

builders; Real

estate; Real

estate service

State of

nature

Ecosystem

extent and

condition

Urban

green space

created.

Potential measures could

include:

• Green plot ratio;

• Urban greening factor;

• Area of tree planting (m

2

);

• Area of a building on which

plants are planted (m

2

);

• Share of area above

threshold for normalised

dierence vegetation

index; and

• Number of areas of

sections of planted trees of

more than 100m

2

created.

Ong (2003);

The Ecology

Consultancy

(2017); IUCN

Urban Nature

Indexes; HTT

Tokyo Green

Building

Program

for New

Buildings

Engineering &

construction

services; Home

builders; Real

estate; Real

estate service

Response Dependency,

impact, risk and

opportunity

management

General Proportion of materials used

that are recycled and reused

input materials by signicant

categories of raw materials,

renewable materials and

manufactured products (%);

or

Share of total mass of

materials, products and

components/systems for

the new build/refurbishment/

t-out that have been

reused, repurposed or

remanufactured, either from

the building undergoing

demolition, refurbishment,

t-out or from other buildings,

third parties etc. (%).

GRI: G4-

EN2;

UK Green

Building

Council

(2023)

Draft sector metrics

For market consultation and feedback – December 2023

39

Glossary

Term Denition

Deforestation

The conversion of forest to other land use independently of whether human-induced or not.

Explanatory notes:

1. Includes permanent reduction of the tree canopy cover below the minimum 10%

threshold.

2. Includes areas of forest converted to agriculture, pasture, water reservoirs, mining

and urban areas.

3. The term specically excludes areas where the trees have been removed as a result

of harvesting or logging, and where the forest is expected to regenerate naturally or

with the aid of silvicultural measures.

4. The term also includes areas where, for example, the impact of disturbance,

overutilisation or changing environmental conditions aects the forest to an extent

that it cannot sustain a canopy cover above the 10% threshold.

5. The concept of long-term is central to this denition and is dened as ten years.

6. Note that to determine whether the removal of trees from an area is classed as

deforestation, it is necessary to predict the future development of the area. If

new forest trees are established in the near future, the land is classied as forest

throughout the regeneration period. This regrowth is considered ‘reforestation’ and

the full process ‘conversion’. If, on the other hand, a sucient density of trees is

not established in the near future, or if land is converted to other land use, the area

should be considered deforested.

Food and Agriculture Organization (2020) Forest Resources Assessment Terms and

Denitions, Food and Agriculture Organization (2000) Forest Resources Assessment

Denitions of Forest Change Processes.

40

Draft sector metrics

For market consultation and feedback – December 2023

Term Denition

Deforestation-free /

No deforestation

Commodity production, sourcing or nancial investments that do not cause or

contribute to deforestation (as dened by the Accountability Framework).

• No-deforestation refers to no gross deforestation of natural forests, which the

Accountability Framework species as the appropriate policy and goal on this topic

for companies and supply chains.